The accounting record of accrued expenses is a fundamental task for any company, since it allows precise control of the economic obligations that have been generated, but have not yet been paid. These types of expenses are those that have accrued in a certain accounting period, but whose payment will be made at a later time. Therefore, it is important to know how to make the accounting entry of accrued expenses, to guarantee the correct presentation of the company's financial information.

We will present a practical guide to make the accounting entry of accrued expenses, in which we will explain the basic concepts related to this type of expense, as well as the steps to follow for its accounting record. In addition, we will provide practical examples that will help to understand this accounting process more clearly. So if you're a business owner or interested in accounting, keep reading!

Identify accrued expenses that must be recorded in your accounting

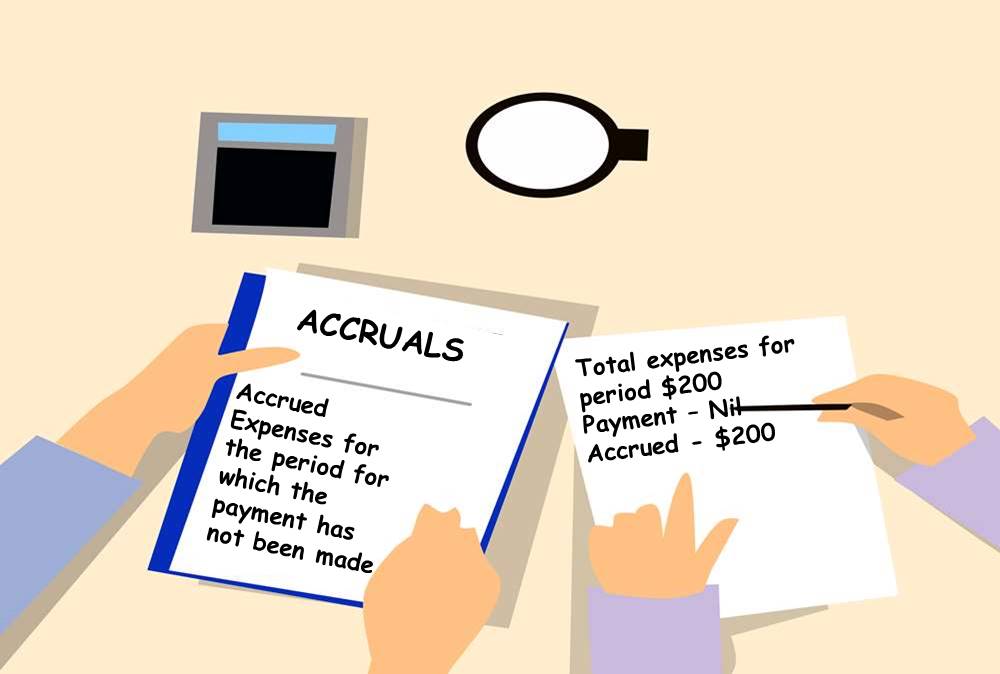

Accrued expenses are those that have been generated in a certain accounting period, but have not yet been paid. This means that the company has an outstanding payment obligation for these expenses .

To identify the accrued expenses that must be recorded in your accounting, it is important to review the documents and invoices that you have received during the accounting period. These documents must prove the existence of a payment obligation, even if it has not yet been made.

Some common examples of accrued expenses are:

- Salaries and social benefits of employees.

- Utilities (water, electricity, gas, etc.)

- Leases.

- Loan interest.

- Taxes to pay.

It is important to note that accrued expenses must be recorded in accounting according to the accrual accounting principle. This means that expenses must be recognized in the accounting period in which they are generated, regardless of whether they have been paid or not.

Once the accrued expenses have been identified , it is time to make the corresponding accounting entry. Here is an example of how to do it:

Example of accounting entry for accrued expenses:

- The accrued expenses account is debited (for the amount of the expense) and the account corresponding to the type of expense is credited (for the same amount).

- The account corresponding to the type of expense is debited (for the amount of the expense) and the suppliers account is credited (for the same amount).

Remember that it is important to consult with an accountant or specialized professional before making any accounting entry, since accounting standards may vary depending on the country and the particular situation of the company.

Review the documents that support the accrued expenses to obtain the necessary information

Before making the accounting entry for accrued expenses , it is important to carefully review the documents that support said expenses. These documents may include invoices, contracts, account statements, payment receipts, among others.

The information you will need to obtain from these documents includes the total amount of the expense, the date it was incurred, a detailed description of the transaction, and the corresponding ledger account.

Identifies the accounting account corresponding to the accrued expense

Once you have reviewed the documents and obtained the necessary information, the next step is to identify the accounting account corresponding to the accrued expense .

The accounting accounts are used to classify and record the different types of financial transactions of a company. Each accrued expense must be assigned to a specific accounting account, according to the nature of the expense.

It is important to note that ledger accounts may vary depending on the accounting system used by the company. Therefore, it is recommended that you refer to the chart of accounts or chart of accounts to identify the correct ledger account.

Make the accounting entry of accrued expenses

Once you have identified the ledger account corresponding to the accrued expense , you are ready to make the accounting entry.

The accounting entry is the accounting record of a financial transaction. In the case of accrued expenses , the accounting entry must include the corresponding accounting account, the amount of the accrued expense and the date it was accrued.

To make the accounting entry, you can use the following format:

- Debit: Ledger account – Accrued expense amount

- Credit: Ledger account – Accrued expense amount

Remember that the debit and credit must be balanced, that is, the total amount of the debit must be equal to the total amount of the credit. This will ensure that the accounting entry is correctly balanced.

Once you have completed the accounting entry, verify that the information is correct and proceed to record the entry in the general ledger or in the company's accounting system.

Making the accounting entry of accrued expenses in an accurate and timely manner is essential to maintain the integrity of the company's accounting records. This will allow you to have adequate financial control and make informed decisions based on updated financial information.

Create a specific ledger account for accrued expenses

In order to make the accounting entry of accrued expenses correctly, it is important to create a specific accounting account for this type of transaction. This account will allow us to keep a detailed control of accrued expenses that have been accrued but have not yet been paid.

The accounting account for accrued expenses can be created within the group of expense accounts, and it is recommended to assign it a number or code that identifies it in a clear and easy to remember way. For example, we could assign the code 6200 for the " Accrued Expenses " account .

It is important to note that the creation of this accounting account does not imply a change in the recording process of accrued expenses , but simply provides us with a more organized and specific way of keeping track of these expenses.

Record accrued expenses in the corresponding accounting account

Once you have created the ledger account for accrued expenses , the next step is to record the accrued expenses in this account. To do this, you must identify the accrued expenses that have been accrued but not yet paid, and allocate the corresponding amount to them.

It is important to take into account that accrued expenses must be recorded in the accounting account corresponding to the type of expense to which they belong. For example, if it is about expenses accrued for services, these must be registered in the accounting account of " Accrued Services Expenses ".

When recording accrued expenses in the corresponding ledger account, be sure to use double entry, that is, you must record both the amount of the expense and the corresponding amount in the accrued expense account .

Update the accounting entry when the accrued expenses are paid

Once the payment of accrued expenses is made , it is necessary to update the accounting entry to reflect this transaction. To do this, you must register the amount paid in the accounting account corresponding to the type of expense and decrease the amount registered in the accrued expenses account .

In this way, you will be reflecting in an accurate and orderly manner the accounting record of accrued expenses and their subsequent payment.

Finally, it is important to carry out a regular review and reconciliation of the accrued expense ledger accounts . This will allow you to identify possible errors or discrepancies in the accounting records, as well as have an updated control of accrued expenses that have been accrued but have not yet been paid.

By performing this review and reconciliation on a regular basis, you will be able to correct any errors or discrepancies in a timely manner, avoiding potential problems in the future.

Record accrued expenses in the accounting entry, using the corresponding accounting account

In order to make the accounting entry of accrued expenses correctly, it is essential to use the corresponding accounting account. This will allow us to keep an adequate record of the expenses and reflect them correctly in our accounts.

The accounting account that we must use to record accrued expenses is the “ Accrued Expenses ” or “ Accrued Expenses ” account . This account is a liability account and is used to record those expenses that have been accrued but not yet paid.

It is important to note that accrued expenses are recorded at the time they are generated, regardless of whether we have not yet made the corresponding payment. This allows us to keep a more precise control of our obligations and obtain a faithful image of our financial situation.

Once we are clear about which accounting account to use, we proceed to make the accounting entry of accrued expenses . To do this, we use the following structure:

Accounting entry of accrued expenses:

- Debit: Account of Accrued Expenses

- Credit: Corresponding Expense Account

On the “Debit” side, we record the amount of the accrued expense, using the Accrued Expenses account . On the "Credit" side, we record the amount of the expense in the account corresponding to its nature, for example, if it is a rental expense, we use the "Rental Expenses " account.

It is important to mention that, in the event that accrued expenses are paid later, a new accounting entry must be made to reflect the payment in the " Accrued Expenses " account and reduce the amount pending payment.

Remember that keeping proper control of accrued expenses allows us to have a clearer vision of our financial obligations and avoid unpleasant surprises in the future.

Be sure to include the date the expense was accrued

It is important to take into account the date on which the expense was accrued in order to make the accounting entry correctly. This date corresponds to the moment in which the obligation to pay for the good or service acquired was generated.

The accounting entry must reflect this date to ensure correct accounting of the expense and comply with accrual accounting principles . In this way, the obligation is properly recorded and avoids distorting the company's financial information.

For this, the <strong> tag must be used in the field corresponding to the record of the accrual date of the expense.

Calculate the amount of the accrued expense and record the amount in the corresponding column of the accounting entry

The first step to make the accounting entry of accrued expenses is to calculate the amount of the accrued expense . This amount represents the expense incurred but has not yet been paid or recorded in the accounting books.

Once you have calculated the amount of the accrued expense, you must record this amount in the corresponding column of the accounting entry. This column is often called " Debit " or " Credit " and is used to record increases in accrued expenses.

It is important to ensure that the amount of the accrued expense is correctly recorded in this column to avoid errors in the accounting records and to ensure the accuracy of the company's financial information.

Remember that the accounting entry is a fundamental tool to reflect the financial movements of a company and keep a detailed record of all transactions. Therefore, it is crucial to correctly record the amount of the accrued expense in the corresponding column of the accounting entry.

To make the accounting entry for accrued expenses , you must calculate the amount of the accrued expense and record this amount in the corresponding column of the accounting entry.

Verify that the accounting entry is balanced, that is, that the debits and credits are equal

To make the accrued expenses accounting entry correctly , it is essential to verify that the entry is balanced. This means that the sum of the debits must equal the sum of the credits .

To check the balance of the accounting entry, it is advisable to use a calculator or a spreadsheet such as Excel . This way, you can add the debits and credits separately and compare the results.

If the sum of the debits is equal to the sum of the credits, it means that the entry is balanced and you can proceed to record the accrued expenses . In the event that there is a difference between the two amounts, it is necessary to carefully review the entry and correct any errors that may have been made.

Remember that a balanced accounting entry is the foundation for accurate and reliable accounting . Therefore, always check that debits and credits are in balance before continuing to record accrued expenses .

Keep a copy of the accounting entry of accrued expenses for your records

When making the accounting entry for accrued expenses, it is important to keep a copy of said entry for your accounting records. This copy will serve as backup and documentation of the transactions carried out.

To save a copy of the accounting entry, follow these steps:

- Identify the accounting entry for accrued expenses : Before saving a copy, it is necessary to correctly identify the accounting entry corresponding to accrued expenses. Verify that the amounts and concepts are correct.

- Create a file in PDF format : To save a digital copy of the accounting entry, it is recommended to convert it to PDF format. This will ensure that the document remains unchanged and is easy to share or print in the future.

- Save the file with a descriptive name : When saving the PDF file, assign a descriptive name that allows you to quickly identify the content of the accounting entry. Use a consistent format to name your files, for example: "AsientoContable_GastosDevengados_month_year".

- Organize your files in a folder structure : To maintain order in your accounting records, it is advisable to create a folder structure that allows you to classify and organize the accounting entry files. You can create folders by year, month, or by transaction type, whatever is convenient for your business.

- Make regular backup copies : Once you have saved a copy of the accounting entry of accrued expenses, it is important to make regular backup copies of your files. You can use cloud storage services or external storage devices to back up your accounting records and ensure their security.

Remember that keeping an adequate record of the accounting entries of accrued expenses is essential for the correct financial management of your company. By following these steps and maintaining an adequate organization of your files, you can always have the necessary documentation at hand in case of audits or accounting queries.

Carry out a periodic reconciliation of the accrued expenses registered in your accounting with the supporting documents

It is important to keep a precise control of the accrued expenses registered in your accounting to guarantee the accuracy and veracity of your financial statements. One way to do this is by performing a periodic reconciliation between the accrued expenses recorded in your accounting system and the corresponding supporting documents.

Periodic reconciliation will allow you to identify possible discrepancies or errors in the accounting records, as well as ensure that all accrued expenses are correctly recorded. This is especially important to comply with current accounting principles and tax regulations.

To carry out the reconciliation, it is recommended to follow these steps:

- Review your accounting records and select the time period you want to reconcile. It can be monthly, quarterly or yearly, depending on your needs and the frequency of your transactions.

- Obtain the supporting documents of the accrued expenses corresponding to said period. These may include invoices, receipts, proof of payment, among others.

- Compare the information recorded in your accounting system with the information contained in the supporting documents. Verify that the amounts, dates and concepts match.

- Identifies and records discrepancies or errors found. This may include unrecorded accrued expenses, duplicate or incorrect records, among others.

- Make the necessary adjustments in your accounting to correct any discrepancies or errors found. These adjustments must accurately reflect the financial situation of your company.

It is important to note that regular reconciliation of accrued expenses will not only help you maintain orderly and accurate accounting, but will also allow you to make more informed financial decisions and avoid potential penalties or problems with the tax authorities.

Remember that each company may have particularities in its accounting process, so it is advisable to consult an accountant or specialist in the area to adapt this guide to the specific needs of your business.

Frequent questions

1. What are accrued expenses?

Accrued expenses are those that have been generated in an accounting period, but have not yet been paid.

2. How is an accrued expense recorded?

It is recorded as an accounting entry in the corresponding expense account and is recognized in the accounting period in which it was generated.

3. When must the accounting entry of an accrued expense be made?

The accounting entry must be made at the end of the accounting period in which the accrued expense was generated.

4. What information is needed to make the accounting entry of an accrued expense?

It is necessary to know the amount of the accrued expense, the corresponding expense account and the date on which the expense was generated.